The return to an office environment - either full-time or more likely with a hybrid working structure - will come us a shock. Not like a daring new haircut or colourful new outfit in the past, but the reappearance of an unrecognisable member of staff. They may look physically similar - albeit having naturally aged a little - but mentally they will be very different having been used to increased flexibility, holding greater responsibility and more control over their working lives.

It will be hard to find the right balance in the future. Employees have been pushing for more freedom over their working hours and working locations for some time and many employers have continued to hold them on a tight leash. The COVID-19 pandemic may have altered the mindsets, but it is easy to make decision when the options are limited by government restrictions and helping to fight against the worst health crisis of modern times. It is a little different when those barriers are removed.

But the cost of not listening to employee needs could come at a high price for employers. In a McKinsey & Company survey earlier this year, over a quarter of respondents said they would consider switching employers if it meant working on-site full-time, and nearly half of employees reported feeling anxious due to lack of clear post-pandemic work arrangements.

As economies start to open up the work from home requests will increasingly be erased from country to country. For businesses, finding a sustainable solution that meets their own and staff needs could prove to be one of the biggest challenges they face in the initial stage of pandemic recovery.

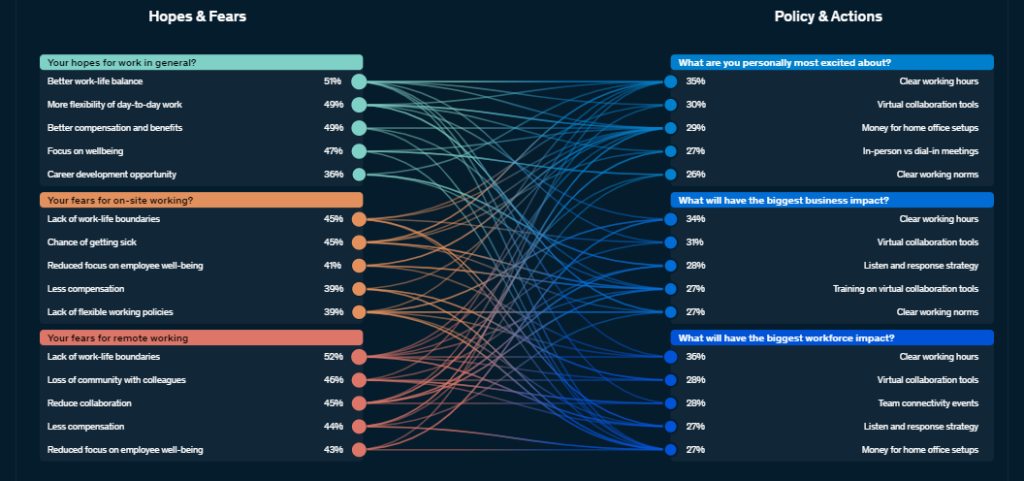

They say 'a picture paints a thousand words'. In this regular section CTC - Corporate Travel Community offers an illustrative insight into a key industry observation or trend, this week highlighting a graphic from the aforementioned McKinsey & Company report that illustrates how employees' hopes and fears match-up with potential post-pandemic policies and actions.

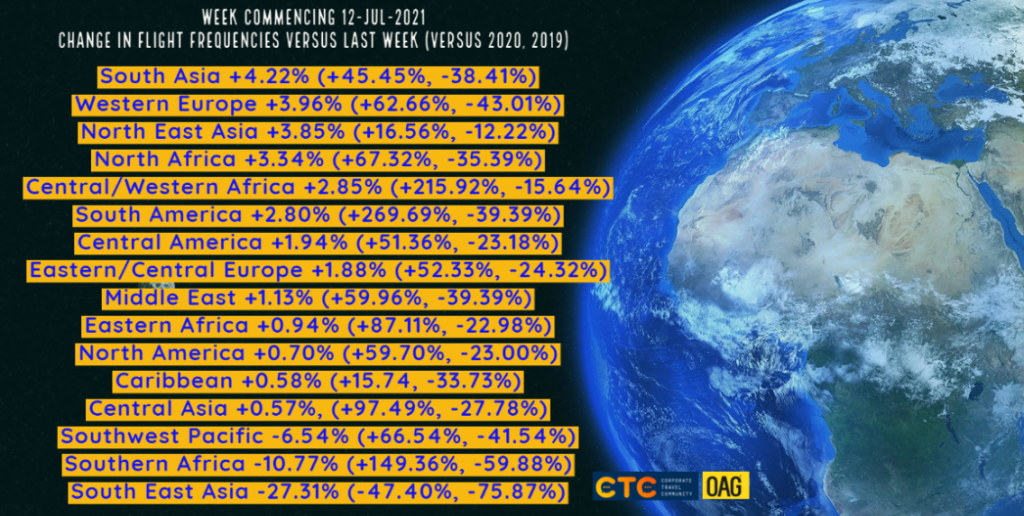

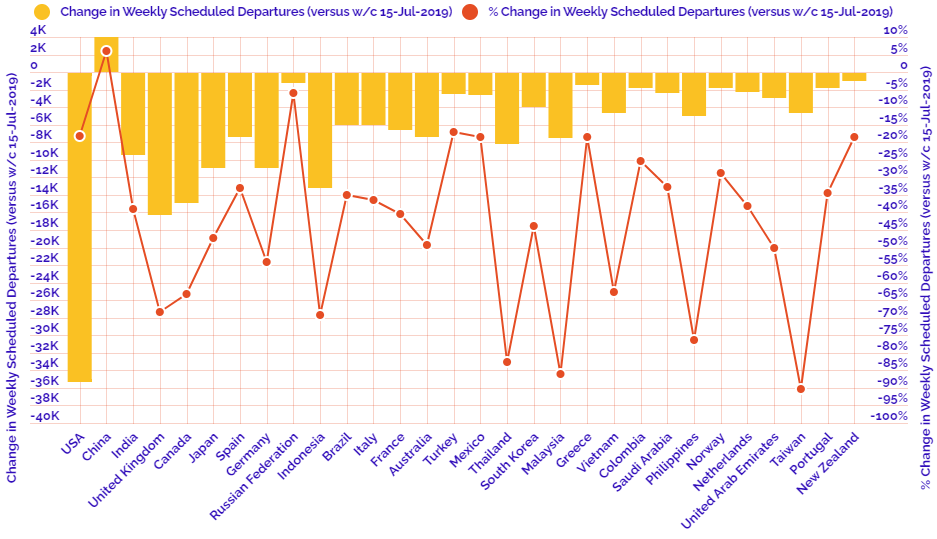

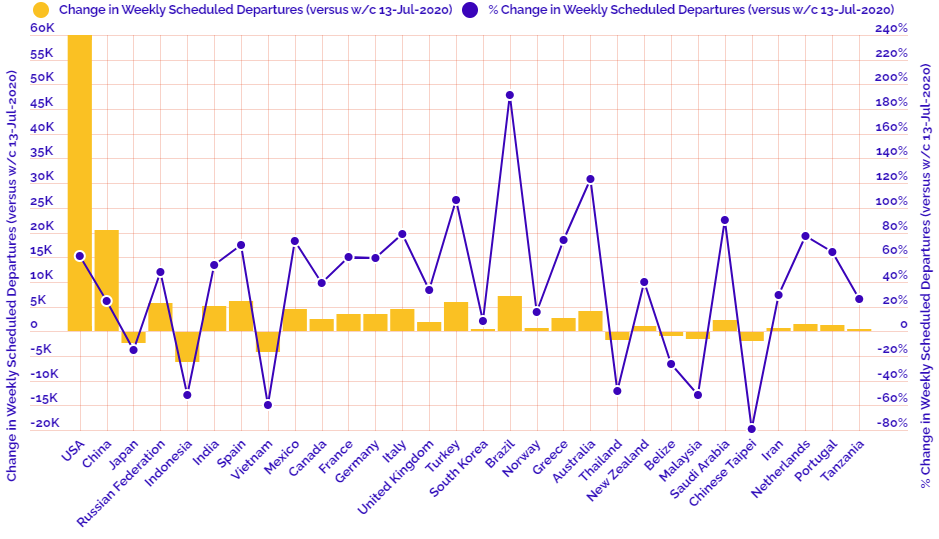

This regular section also now incorporates and expands on the charts produced in the 2020 air capacity series 'Coronavirus Statistics Snapshot'. These are based on an analysis of OAG schedule data and include a weekly look at how the pandemic is impacting global flight levels in the world's largest markets; a week-on-week and year-on-year comparison of flight departures by geographical region and a look at how weekly capacity is trending: the latter comparing levels to 2020 and also to the 2019 baseline performance.

HEADLINE FIGURES FOR WEEK COMMENCING 12-Jul-2021:

Departure frequencies up+1.04% versus last week; up+43.14% versus 2020 and down -31.94% versus 2019.

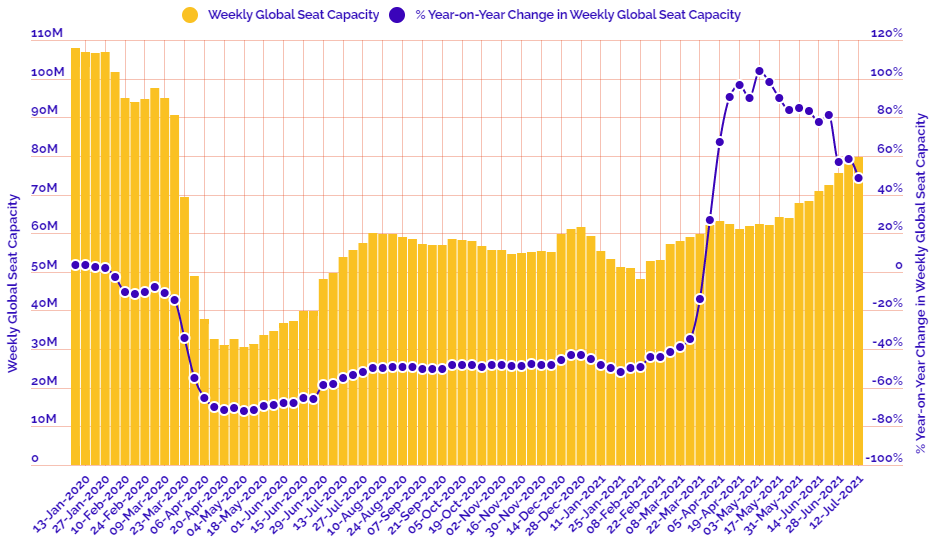

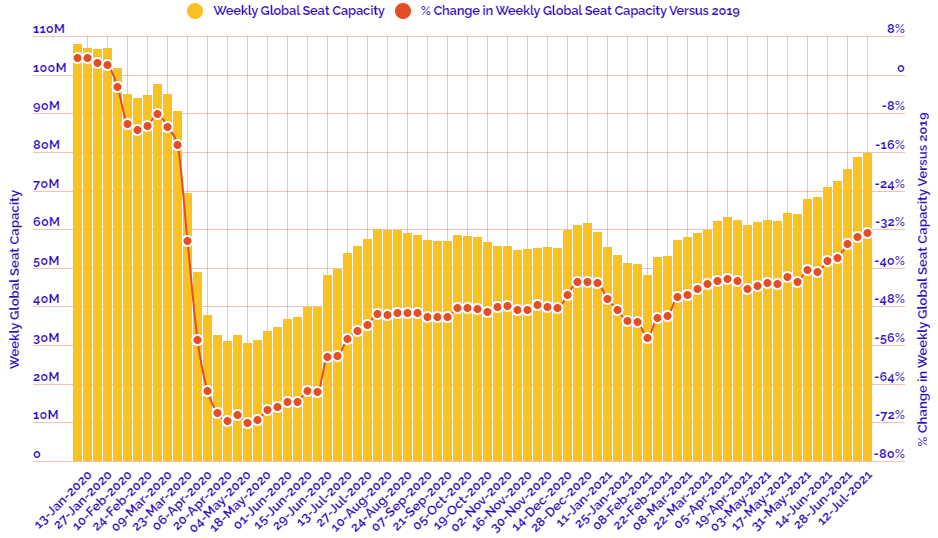

Seat capacity up +1.52% versus last week; up +48.34% versus 2020 and down -32.86% versus 2019.

CHART: Week-on-week change in flight departures by region

CHART: Year-on-year weekly departures performance for world's top 30 markets versus 2019

CHART: Year-on-year weekly departures performance for world's top 30 markets versus 2020

CHART: Departure capacity trends with year-on-year performance

CHART: Departure capacity trends versus 2019

CHART: The world's biggest aviation markets by departure seats