Charting the trends – the strongest global domestic markets have helped boost air travel; China, Russia and South Korea have all now returned to growth

26 October, 2020

With border restrictions and quarantines a key aspect of any government's arsenal against COVID-19 spread international travel has continued to be weakened and as expected domestic travel is recovering before international. There are a number of success stories, but also just because a country has a strong domestic market does not mean it is guaranteed to see a similar scale of recovery. In the current challenging marketplace there are far too many variables.

UNWTO data shows that in 2018, around nine billion domestic tourism trips were made worldwide - six times the number of international tourist arrivals (1.4 billion in 2018). This is certainly cushioning the impacts of the COVID-19 fuelled crisis for a number of destinations helping them recover from the economic impacts of the pandemic, while at the same time safeguarding jobs, protecting livelihoods and allowing the social benefits tourism offers to also return.

In most destinations, domestic tourism generates higher revenues than international tourism. In OECD nations, domestic tourism accounts for 75% of total tourism expenditure, while in the European Union, domestic tourism expenditure is 1.8 times higher than inbound tourism expenditure, according to a UNWTO briefing note on the subject.

It highlights that globally the largest domestic tourism markets in terms of expenditure are the United States with nearly USD1 trillion, Germany with USD249 billion, Japan USD201 billion, the United Kingdom with USD154 billion and Mexico with USD139 billion.

They say 'a picture paints a thousand words'. In this new regular section CTC - Corporate Travel Community offers a graphical insight into a key industry observation or trend. In this fourth edition we use OAG schedule data to look at the recovery of domestic air travel and how individual country markets have performed to date in 2020.

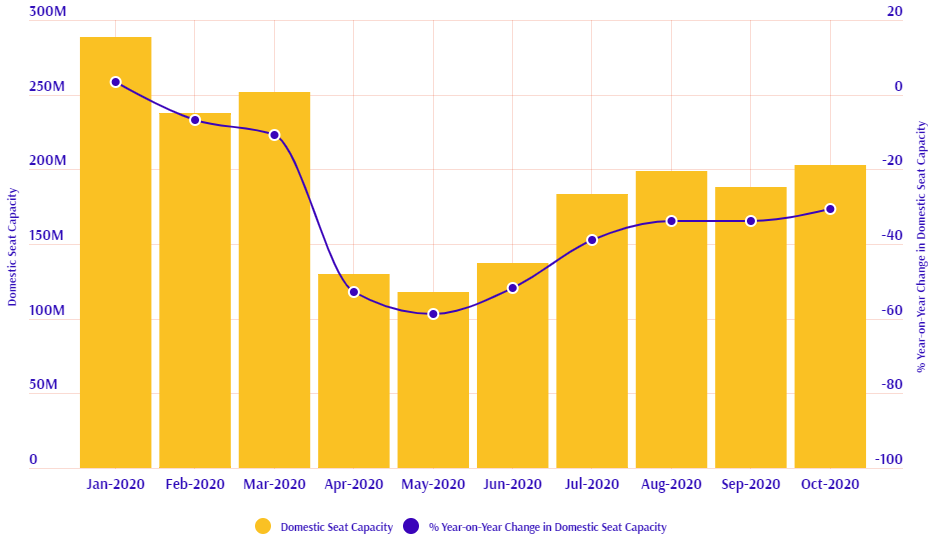

When looking at global domestic air travel alone, the impact of COVID-19 does not look so severe. The monthly decline in domestic capacity fell to just 40% of last year's levels in its worst month (May-2020) but has subsequently recovered to a position that global levels have been down just a third on last year in Aug-2020 and Sep-2020, improving still further in Oct-2020, based on completed and projected schedules (Source: CTC - Corporate Travel Community and OAG; data: w/c 19-Oct-2020)

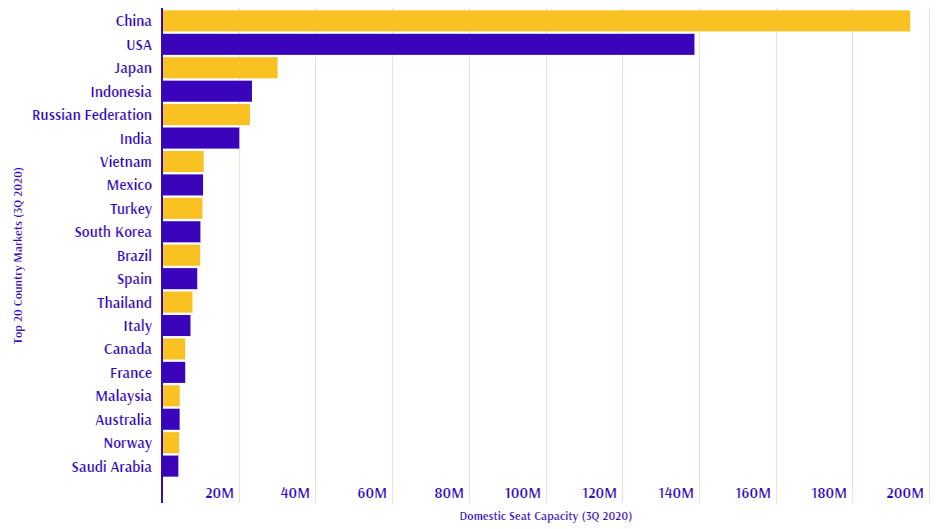

The impact of COVID-19 has highlight the importance of a strong domestic market, but still wider lockdowns and internal travel restrictions have impacted the performance of many of the world's largest. China's quick recovery has been clearly helped by its strong domestic market, others such as the emerging market of Vietnam have gained from strong domestic air travel options (Source: CTC - Corporate Travel Community and OAG; data: w/c 19-Oct-2020)

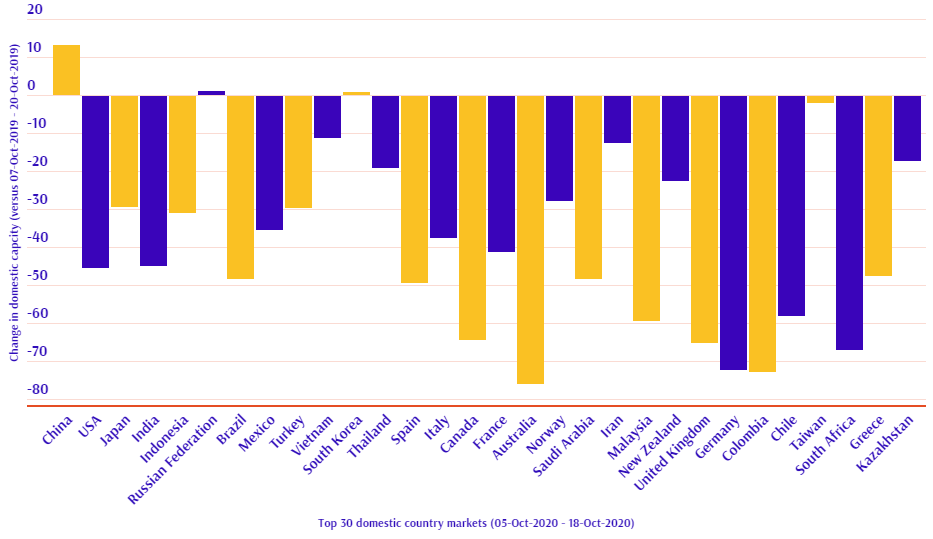

A data snapshot comparing the first two full weeks of Oct-2020 against Oct-2019 shows that China, Russian Federation and South Korea all have a larger domestic market this year. At the other end of the spectrum major domestic markets such as Australia, Germany and Colombia continue to see capacity declines of more than -70% year-on-year (Source: CTC - Corporate Travel Community & OAG; data: w/c 19-Oct-2020)