What is significant is that +7.9% was the lowest recorded annual growth rate of the decade, a ten year period that had seen annual passenger traffic grow from just under 267 million in 2010. Despite the softening growth, 2020 was set to be another year of significant growth for aviation in China. But, over those final few weeks of 2019 the COVID-19 novel coronavirus outbreak began in Wuhan and now it is a very different story.

As intelligence specialist OAG noted when analysing its own schedule data, at the start of the year China was the third largest international aviation market in the world; but now ranks 25th, just behind Portugal and slightly ahead of Vietnam. As it says: "some change in just a few weeks!" A flu like virus will prove that when China sneezes, the world catches a cold.

While containment efforts have attempted to limit the international spread, more than 30 countries around the world have now recorded cases of COVID-19. Most fatalities are limited to the city and region where it originated, but are now also being recorded across the wider world. The impact on China's economy is obvious, but that is also spreading like the virus across the world.

Oxford Economics, a leading economic forecaster, has warned that the spread of the virus to regions outside Asia would knock -1.3% off global growth this year, the equivalent of USD1.1 trillion in lost income. The consultancy said its model of the global economy showed the virus was already having a "chilling effect" as factory closures in China spilled over to neighbouring countries and major companies struggled to source components and finished goods from the far east.

Meanwhile, initial assessment of the impact of the outbreak from the International Air Transport Association (IATA) shows a potential -13% full-year loss of passenger demand for carriers in the Asia-Pacific region.

The growth for the region's airlines was forecast to be +4.8%, meaning the net impact will be an -8.2% full-year contraction compared to 2019 demand levels. In this scenario, that would translate into a USD27.8 billion revenue loss in 2020 for carriers in the Asia-Pacific region-the bulk of which would be borne by carriers registered in China, with USD12.8 billion lost in the China domestic market alone.

In the same scenario, IATA says carriers outside Asia-Pacific are forecast to bear a revenue loss of USD1.5 billion, assuming the loss of demand is limited to markets linked to China. This would bring total global lost revenue to USD29.3 billion (-5% lower passenger revenues compared to what IATA forecast in December) and represent a -4.7% hit to global demand. In December, IATA forecast global RPK growth of +4.1%, so this loss would more than eliminate expected growth this year, resulting in a -0.6% global contraction in passenger demand for 2020.

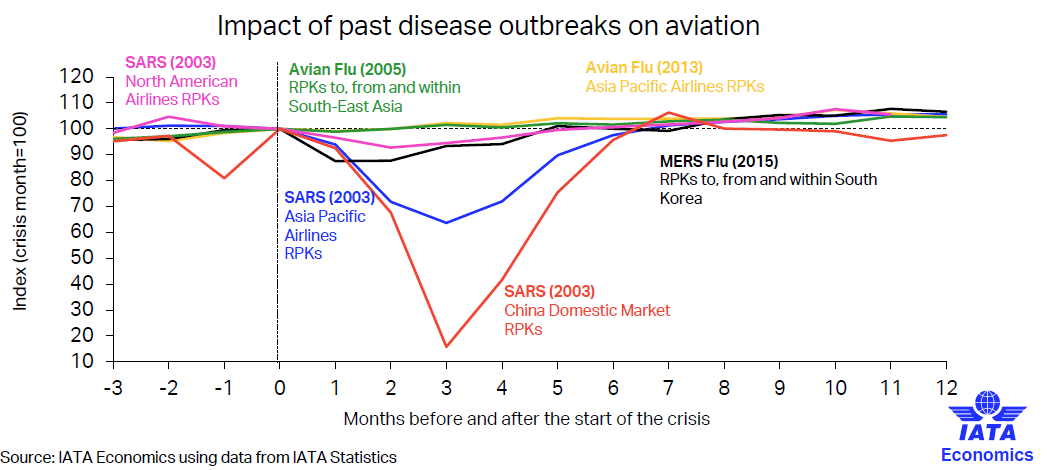

CHART - IATA's guidance is based on analysis of previous disease outbreaks which have peaked after one to three months and recovered pre outbreak levels in six to seven months Source: IATA Economics

Source: IATA Economics

These estimates are based on a belief that COVID-19 has a similar V-shaped impact on demand as was experienced during SARS. That was characterised by a six-month period with a sharp decline followed by an equally quick recovery. In 2003, SARS was responsible for the -5.1% fall in the RPKs carried by Asia-Pacific airlines.

The estimated impact of the COVID-19 outbreak also assumes that the centre of the public health emergency remains in China. If it spreads more widely to Asia-Pacific markets then impacts on airlines from other regions would be larger.

It is premature to estimate what this revenue loss will mean for global profitability. "We don't yet know exactly how the outbreak will develop and whether it will follow the same profile as SARS or not," says IATA.

Governments will use fiscal and monetary policy to try to offset the adverse economic impacts and some relief may be seen in lower fuel prices for some airlines, depending on how fuel costs have been hedged. What is obvious is that global passenger demand will see its first decline since the SARS crisis of 2003.

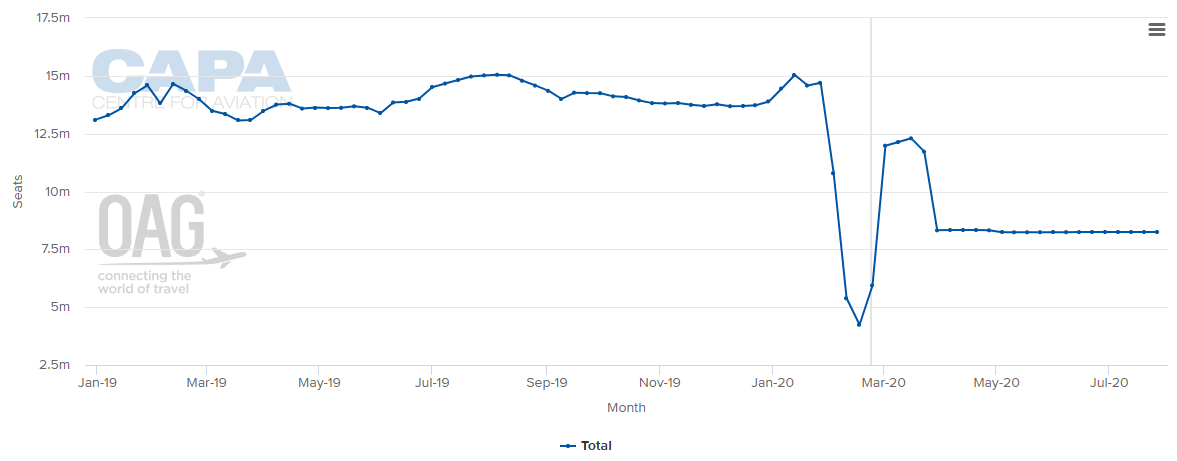

CAPA - Centre for Aviation analysis of OAG schedule data highlights the collapse of domestic air capacity in China over the first quarter of 2020 and how this week could potentially mark the first week of growth since late Jan-2020.

CHART - Analysis of China domestic schedules suggests a V-shaped coronavirus impact, but this could also indicate a U-shaped scenario based on how quickly capacity recovers to previous levels Source: CAPA - Centre for Aviation and OAG

Source: CAPA - Centre for Aviation and OAG