The South African market looks very different currently with the suspension of flights at South African Airways and Comair and Airlink's managing director and CEO Rodger Foster believes that difference will develop in scale as the market void is quickly filled. "When SAA and Comair come back, it will be a completely different market, with a different set of competitors [with] global strength".

When he describes global strength he refers to a range of interline agreements, a method that Airlink is adopting to maximise the strength of its local network to support the major foreign airlines serving just South Africa's largest markets.

Airlink signed an interline agreement with Qatar Airways earlier this month under which it will provide connectivity via Cape Town and Johannesburg to more than 25 domestic and more than 20 regional destinations in southern Africa. This was followed days later with a similar deal with Emirates Airline covering similar markets.

Mr Foster says this will not be the end of the marketing agreements and confirms the airline is in discussions with four African airlines and "at least three major global airlines among the global top 10" regarding further potential interline agreements. Mr Foster said discussions also include potential codeshare and cargo interline arrangements.

Airlink may be a small regional carrier in the scale of things, but it is thinking big to safeguard its own future and take advantage of the opportunity that the void in South Africa is presenting.

ABOUT

SA Airlink, trading as Airlink, is a privately-owned regional airline based in Johannesburg, South Africa that operates scheduled services to destinations across South Africa. The airline also offers international services to destinations in Zimbabwe, Madagascar and Zambia.

GLOBAL RANKING (as at 26-Oct-2020)

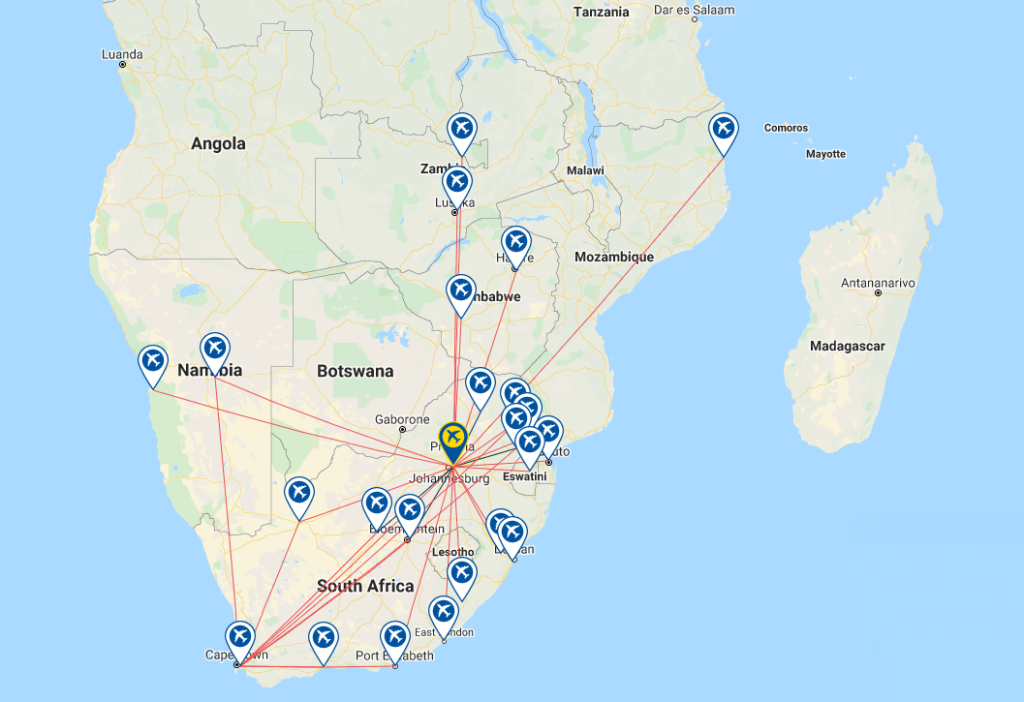

NETWORK MAP (as at 26-Oct-2020)

DESTINATIONS (as at 19-Oct-2020)

CAPACITY SNAPSHOT (versus same week last year)

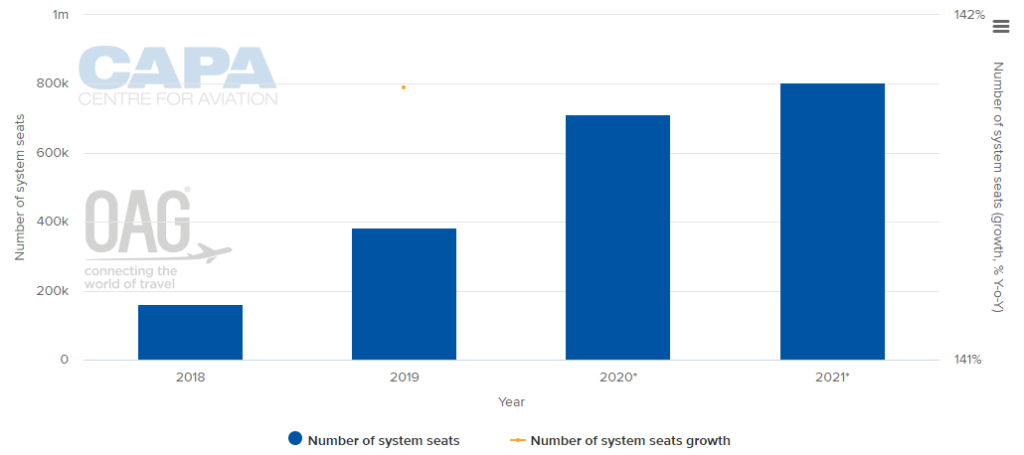

ANNUAL CAPACITY (2012-2021*)(NOTE:The values for this year are at least partly predictive up to 6 months and may be subject to change)

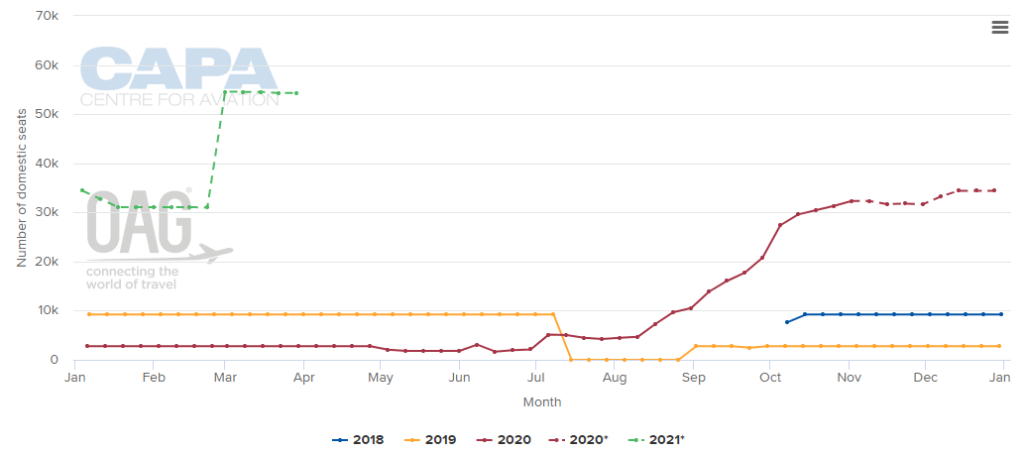

WEEKLY DOMESTIC CAPACITY (2017 - 2020*)(NOTE:The values for this year are at least partly predictive up to 6 months and may be subject to change)

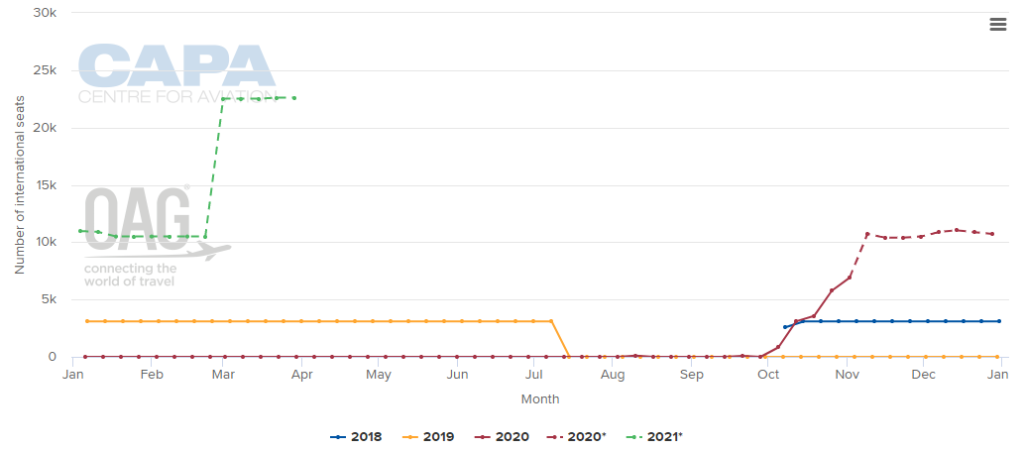

WEEKLY INTERNATIONAL CAPACITY (2017 - 2020*)(NOTE:The values for this year are at least partly predictive up to 6 months and may be subject to change)

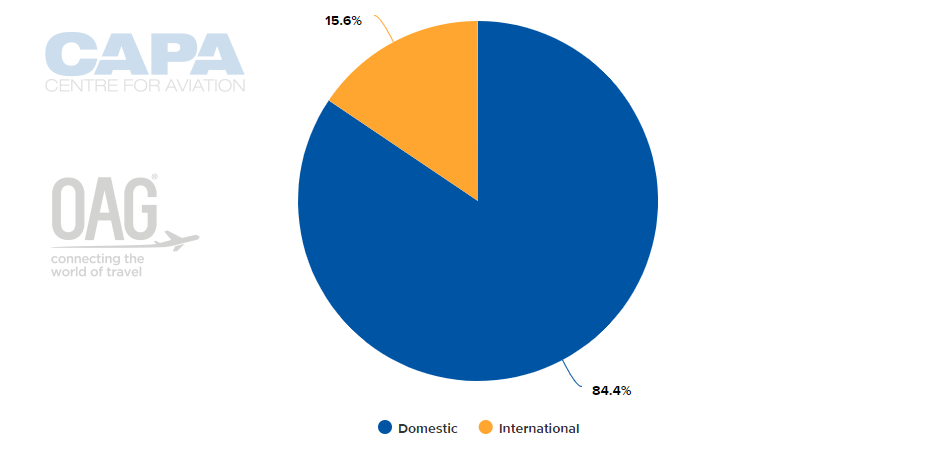

CAPACITY SPLIT BETWEEN DOMESTIC AND INTERNATIONAL OPERATIONS (w/c 26-Oct-2020)

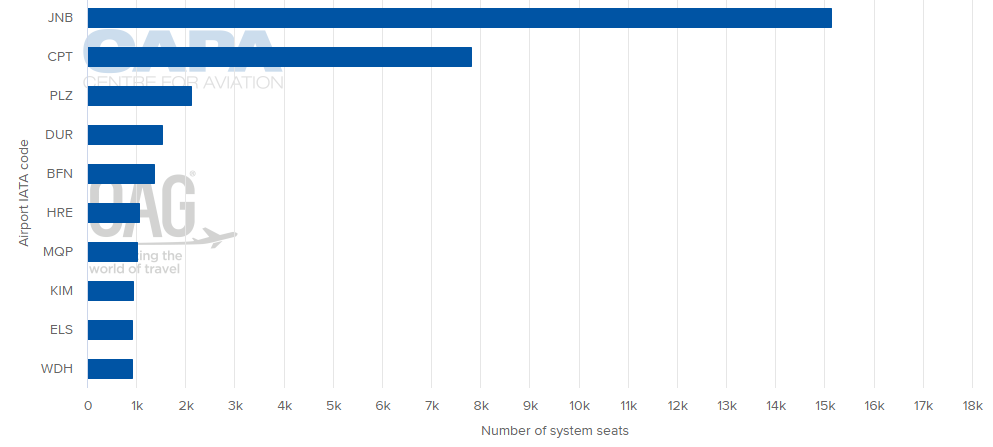

LARGEST NETWORK POINT (w/c 26-Oct-2020)

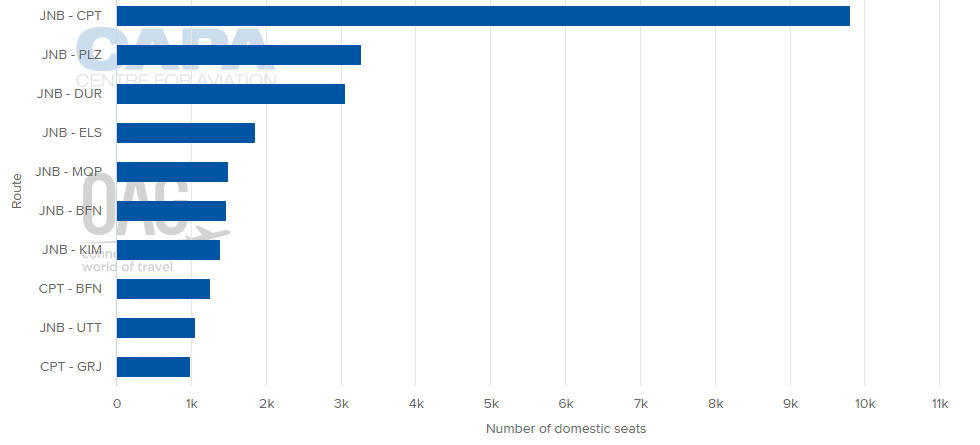

BUSIEST DOMESTIC ROUTES BY CAPACITY (w/c 26-Oct-2020)

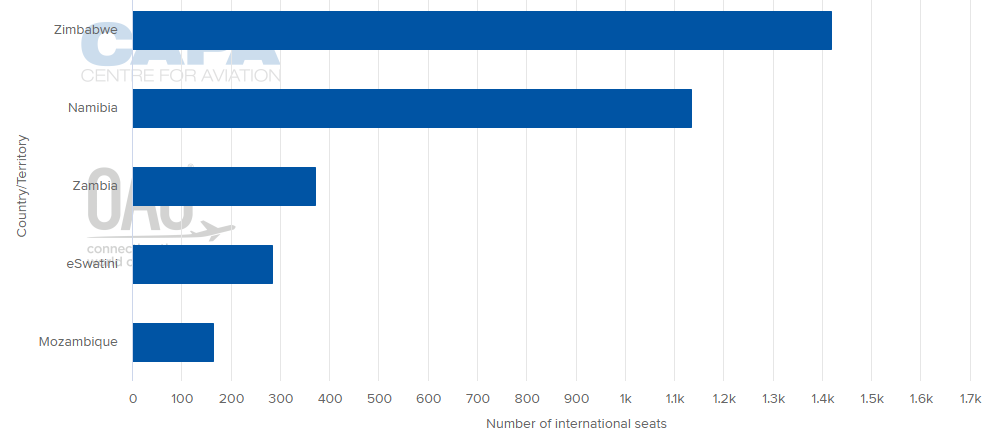

LARGEST INTERNATIONAL MARKETS BY COUNTRY (w/c 26-Oct-2020)

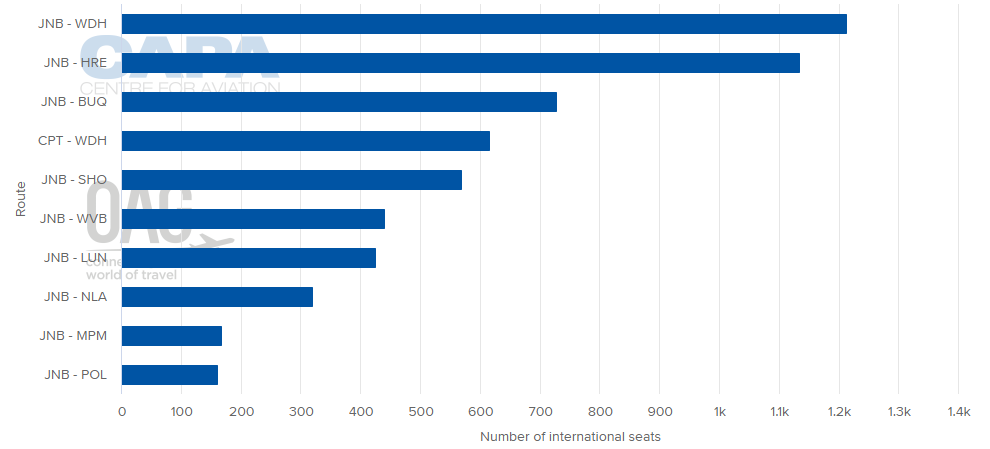

BUSIEST INTERNATIONAL ROUTES BY CAPACITY (w/c 26-Oct-2020)

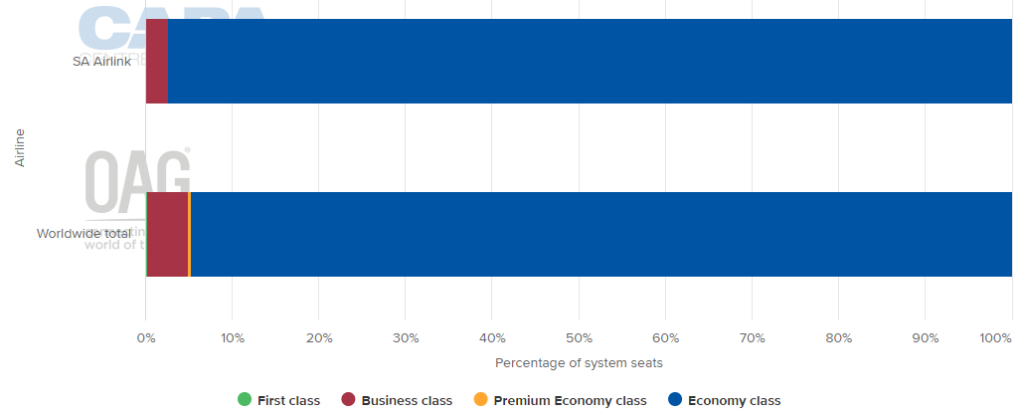

DEPARTING SYSTEM SEATS BY CLASS (w/c 26-Oct-2020)

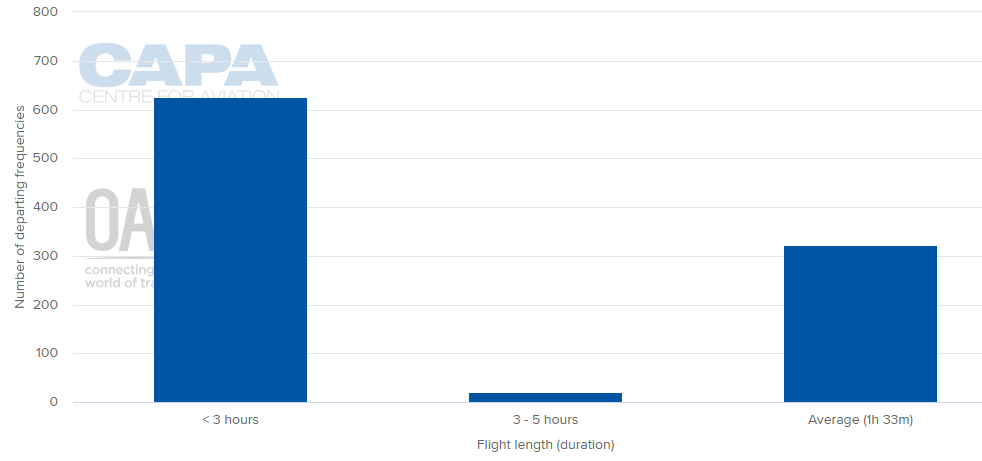

AVERAGE FLIGHT LENGTH (w/c 26-Oct-2020)

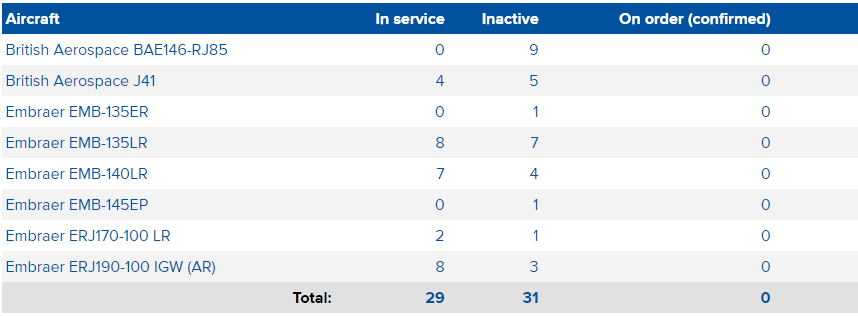

FLEET SUMMARY (as at 26-Oct-2020)

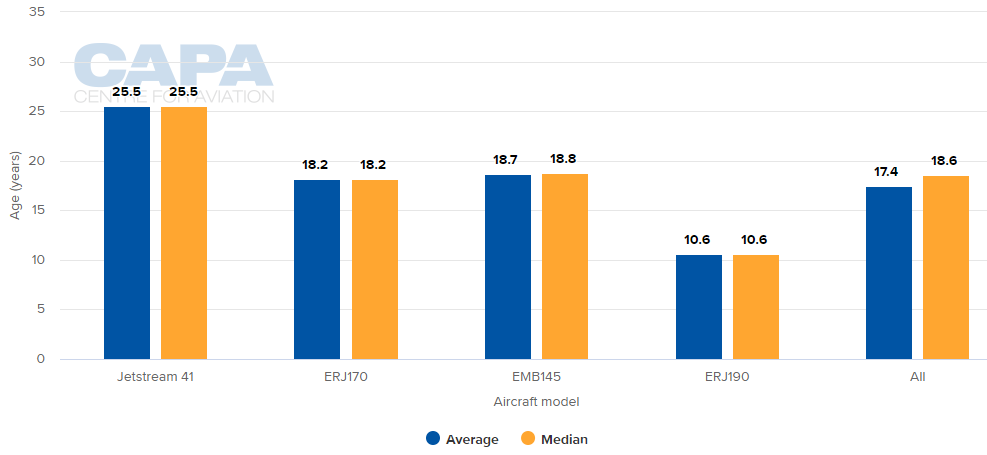

AVERAGE FLEET AGE FOR IN-SERVICE AIRCRAFT (as at 26-Oct-2020)

MORE INSIGHT...

CAPA Live: COVID-19 crisis could prompt overdue change in Africa

American Airlines and United: high hopes for Africa in 2020

Southern Africa airlines need liberalisation and scale to achieve sustained profitability